Whitepaper: Overcoming today's supply chain disruptions

Introduction

Everyone is impacted by supply chain issues nowadays. Chip shortages(How Long Will the Chip Shortage Last?, n.d.), port closures or not enough truck drivers, it feels as the supply chain experiences an additional, unexpected problem nearly every day. These topics have been on top of the news coverage recently. Everyone experienced toilet paper(Helper & Soltas, Evan, n.d.), masks or test shortages at the start of the pandemic and can well relate to similar problems in industry.

While order book for industrial companies either are robust or show increasing order volume and value, part shortages and the other supply chain issues inhibit the companies from realizing the orders. Increasing order volumes lead to further capacity shortages in production for some suppliers, not enough truck drivers lead to transport bottlenecks, port closures lead to transport delays, which require more ships and containers, which are not available (Attinasi et al., 2022).

In this whitepaper, the factors leading to the existing supply chain disruptions are identified. Based on electronic components, the complexity of the supply chain and its impacts on the supply situation of products is analyzed in detail. As electronics are part of nearly every product nowadays, the problems in the electronic supply chain highlight many existing problems. Different solutions for overcoming the difficulties are presented and their impact is discussed.

Reasons for the supply chain disruptions

In the actual situation, a company deals with many suppliers and various problems with different suppliers. Chinese suppliers have difficulties in delivery, as some areas are affected by Covid-shutdowns, the chip supply chain is having problems with capacity bottlenecks in the long lead-time production supply. Capacity-constrained suppliers quote a much longer lead-time or less volume than originally scheduled. Limited material supply leads to higher cost for the supplier, why they ask for higher prices. Transport problems (Wendler-Bosco & Nicholson, 2020) add extra delays. When one part of a product is late, a product cannot be produced and the other parts are delivered on time and increase inventory value. Delays in delivery for one part of a product lead to increased inventory for the other materials.

Due to the supply problems and the additional delays, companies will record less revenue in a period. They are impacted twofold, less revenue on the top line and higher costs on the bottom line.

A few key external factors that impact supply problems lead to numerous supply chain problems. Many different factors have a negative influence on the supply chain. While standard risk mitigation strategies in the supply chain have been increasing inventory, requesting more supply in a capacity constrained market will not work and increases lead-time further. In order to manage the supply chain problems, the different external factors and the resulting supply problems have to be managed properly (Figure 1).

Figure 1: Influence of external factors on supply chain problems

The pandemic has had and still has a major impact on the supply chain. Sick employees are either not at work or employees suffering from Long Covid are not fit for many tasks anymore, requiring new hires and training. Productivity suffers with new workers. Through factory closures, like the recent Covid shutdowns in China in Shanghai, many factories have completely reduced output. Missing truck drivers (Ji-Hyland & Allen, 2022) or port closures have impacted transport capacity. Political unrest due to strikes or civil war like situations typically have similar effects.

Travel restrictions limit international business travel. Less travelers means less flight and this reduces air cargo space, reducing freight room for fast transport. Participating at fairs to find new suppliers or customers, visiting customers and suppliers, engineering meetings, supplier quality audits are more difficult and time consuming. The travel limitations reduce the trust levels that are needed between the supply chain partners.

Natural disasters, such as earthquakes or tsunamis, may affect production capacity. Cyber-attacks on companies (‘til the Next Zero-Day Comes | Safety-Critical Systems EJournal, n.d.) led to closing production facilities. Problems in infrastructure - broken bridges, cranes in ports to reduce train networks for freight transport - hinders transport and will inhibit the global competition for lowest labor costs and will lead to price increases. The external factors lead to supply chain problems and companies need to monitor these elements in order to avoid supply chain disruptions.

Chip shortage – one example for the supply chain disruptions

Electronic components, commonly referred to as chips, demonstrate the supply chain problems (Weathering the Chip Shortage Requires Future-Proofing Supply Chains, n.d.) well. All products with their electronic devices need these components on their printed circuit board to function. State-of-the-technology electronic components are produced with a lead-time of 15 weeks (“8 Things You Should Know About Water & Semiconductors,” n.d.).

Figure 2: Semiconductor 3 months average sales trend (Data source SIA)

The overall sales volume for semiconductors (Figure 2) has always been very cyclic(Ravi, 2022). If customer markets go down, e.g., during the financial crisis of 2009, the semiconductor business follows suit, if the market of products goes up, the electronic component production is at least a quarter ahead of the rise, making the market a good indicator for expected market behavior. During the last years, the semiconductor producing companies kept running at 95% production capacity, so well above the planned limit of 80%. As new semiconductor plants take 3 years from idea to production, adding semiconductor supply capacity is slow compared with the demand fluctuations.

Chips are based on different types of semiconductor production equipment. This equipment needs to be available that is mostly defined by the size of the wafer and minimum feature size, with the wafer becoming bigger and the features becoming smaller. Typically, all equipment for the different steps for chip production are integrated in one plant. A chip plant is dedicated to a wafer size plus the minimum feature size limiting it to certain chips to produce. New production sites are directed at the newest technology and typically cost more than 2 billion USD for a plant. At the same time, when demand dwindles for older technology, the old plants will be closed and companies need to find either new suppliers, which still offer the technology, or find different parts using a more future-proof production. Chip production is also defined by component type, such as a microprocessor or a memory chip. If component design ages, old plants have been closed (see above) and new plants require a different design for the smaller feature sizes.

The chip production is therefore requiring both good long-term planning for the investments in new plants and a medium-term planning for forecasting production for the next quarters based on the demand for different types of chips and available production technology. Events such as the 2009 financial crisis or the 2020 Covid situation with negative business outlook will stop plans for long term investments in new plants severely limiting long-term capacity growth and availability of the next generation production technology that chip designers had relied on. Reduction in forecast numbers from the customers will lead semiconductor producers to postpone investments, as the costs for idle plants are very high. The semiconductor industry cannot deal well with bad forecast accuracy and shifts in demands between different technologies.

The existing chip bottleneck is based on poor forecasting at the beginning of the Covid pandemic and higher demand for chips for IT and telecom products used in the pandemic leading to a full capacity production. The semiconductor sales increased over 25% between 2020 and 2021, surpassing maximum sales of 2019, leading to longer lead-time and not enough available production capacity on the market, resulting in chip shortages.

Product diversity – the next problems with the electronic components

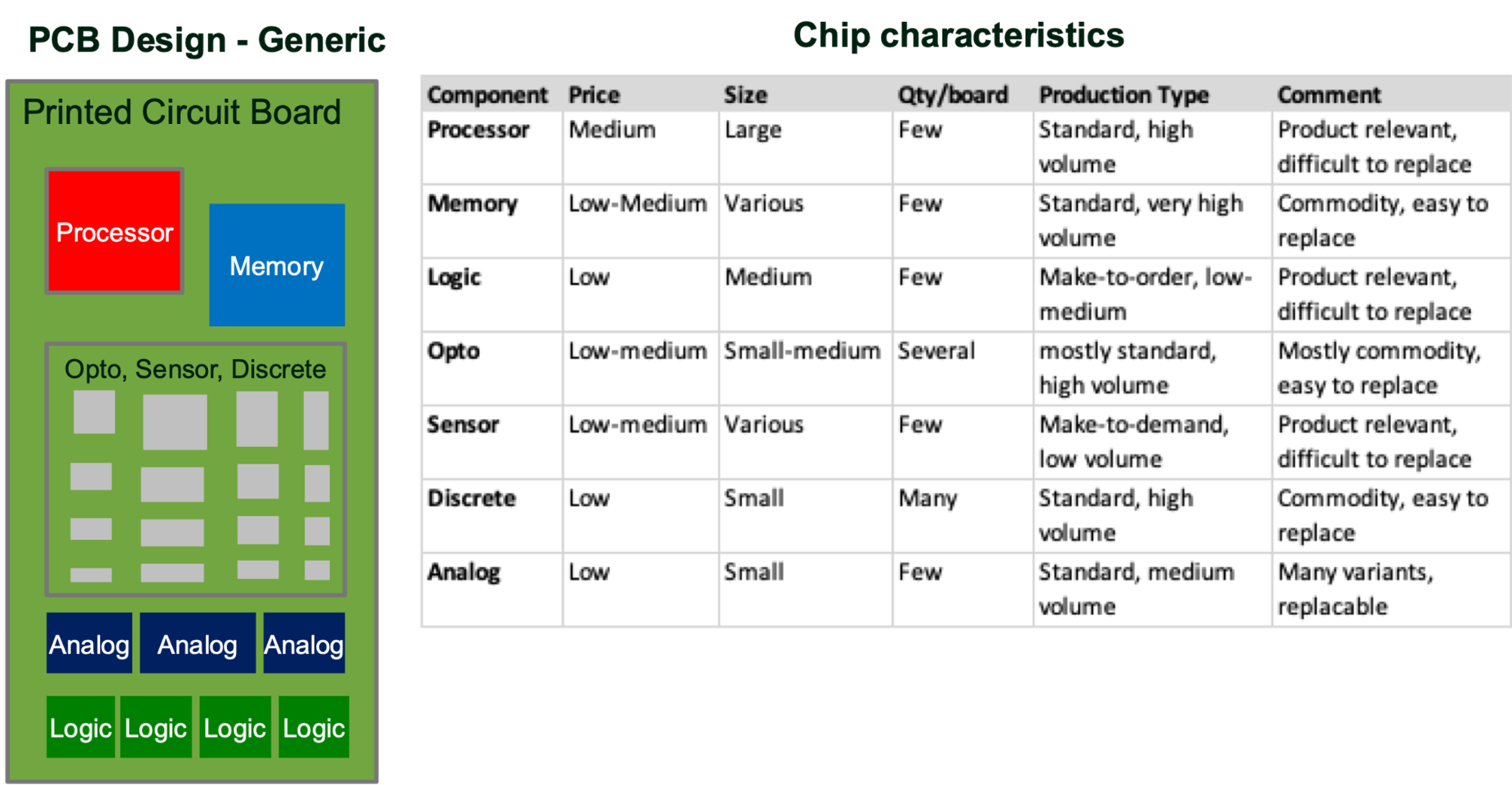

When electronic designers create a new printed circuit board (PCB), chips available on the market will be selected. Typically, an interface, such as a connector for data and some power supply circuitry is added as well, making the PCB a complex assembly.

Figure 3: Structure of a printed circuit board

Figure 3 shows a generic structure of a printed circuit assembly consisting of a board and many different components. The system will typically consist of a processor and some memory chips, some chips for logic processing and many chips for optoelectronic (such as LEDs), sensors or discrete functions. Special boards also require a limited number of analog chips for particular tasks. All these components need different production technology, so they typically require different chip plants with different supply constraints.

Figure 4: Shipped units and sales of opto, sensor and discrete components

Figure 4 describes some of the root causes for the chip problem further. Optoelectronic, sensor and discrete components (OSD) are only 17% of the total sales volume, but are responsible for more than 70% of the shipped units. The OSD components compete typically for limited capacity and other products that can pay higher prices, so these components will not be produced as priority.

Comparing the long-term forecast to the actual sales last year, there was a forecast error of 23% for OSD components, leading to high volume pressure on the manufacturers. If semiconductor production volumes are fully booked and the demand increases, new orders are added only using free capacity at the end of the order load, leading to long lead times.

Impact of chip disruptions on the supply chain

Figure 5: Typical electronic product supply chain

In the typical electronic product supply chain (Figure 5), the company selling the products to the end market may have the design authority for the product, a module, the PCB integrated in the module with all needed components and for a limited number of special chips. The producer will be responsible for the functionality and will specify the module, the PCB and the components. In the normal operation of business, there are roughly 2 weeks for the supply of new modules to the producer. The next levels in the supply chain – module manufacturer and PCB manufacturer –hold sufficient levels of inventory to cover the longer delivery times from their suppliers.

When the product is expected to sell, the producer will provide a forecast to the supplier of the module, which in turn will send a forecast to the PCB and this will eventually end at the chip manufacturer. This semiconductor company needs a good demand overview for at least 6 – 12 months to plan their production.

When demand now exceeds the forecast, the supply chain will first use the buffer inventory but then will increase orders to their suppliers. For the PCB assembler, this increased demand may meet one or more capacity constrained semiconductor producers. This capacity constraint will lead to doubled or tripled lead-times. Much higher lead-times will run any buffer inventory in the supply chain empty. This leads to supply problems for the PCBs and the modules and these companies will increase inventory to buffer these new bottlenecks, adding further demand to an already troubled supply chain.

When the PCB manufacturer increases the lead-time to the module manufacturer by many weeks due to increased chip delivery times, the producer will likely not accept this delay. A lot of information exchange will happen to understand which components and which supplier lead to the delivery problems. The designers at the producers identify if the component can be exchanged easily and supply from other semiconductor vendors can be used to reduce lead-time. This problem resolution may take 2 weeks. The new component must be qualified during first delivery with extra delays. Chip brokers are also available to sell excess inventory from other PCB producers at a premium. All these activities require extra effort and a lot of coordination. The results will be delays in the delivery and often higher costs as well. With the capacity bottlenecks in the semiconductor industry, a company will face many different components with supply problems. The overall result is an unstable supply chain leading to late deliveries and eventually to stock-outs in retail, thus impacting turnover. Semiconductor production capacity issues, transport bottlenecks, blocked transport ways, natural disasters and labor shortages due to the pandemic together have led to more additional variations in the chains in the last year, than the buffers could cope with. The results are the widely reported disruptions in the supply chain.

Solving supply chain disruptions

Figure 6: Possible solutions for supply chain disruptions

Figure 6: Possible solutions for supply chain disruptions

The actual situation requires many changes in the supply chain (Figure 6). Immediate actions ensure material supply and production. This is firefighting. Short-term actions get the supply chain out of the crisis mode. The long-term actions avoid the problems in the future.

In each time horizon, different actions will improve the situation and companies can pick which actions will help them in their particular situation. The work on the different horizons may complement each other or build on one another.

Manage supply risks

Figure 7: Supply risks and item type matrix

Figure 7: Supply risks and item type matrix

The Kraljic matrix(Caniëls & Gelderman, 2005) is used as a key supply risk management tool. It typically separates the purchasing portfolio by supply market risk. The risk criteria include the number of different suppliers available for specific parts, knowledge about capacity or material problems at the supplier, long lead-times or low on-time delivery. Managing disruptions clearly has a supply market risk dimension, but not securing the part supply will inhibit future sales plus increase cost for switching suppliers, impacting the profit. For disruption management, profit impact is a key prioritization metric.

A standard part adhering to international norms, such as a screw, can be exchanged more easily and faster than a catalog part from only one supplier with no alternative. Some parts are low risk commodities that can be sourced from different suppliers. For other parts, suppliers produce to a company drawing –classified as company specific parts. Depending on the drawing specifications and the technical capabilities of the suppliers, there are many sources of supply available for this part or only a few. Sometimes, only one supplier can produce the part to specifications. The classification of sole, single or at least dual sources describes the supply risk that a company has created for its purchases for company specific parts.

Sole sources of supply represent higher risks than multiple sources. A company needs to monitor parts from sole or single sources. The risk is higher for company specific parts, as for standard parts.

Managing supply market risks and part types minimizes disruptions. For the key areas, specific measures need to be implemented to avoid the supply risks:

For sole suppliers, alternative suppliers need to be found and qualified.

For single sources of supply, alternative suppliers need to be (re-)qualified.

For company specific parts, RFQs need to be sent out to understand the supply situation.

The total risk is a multiplication of market supply risks and part type risks. Based on the highest risks, companies track many issues. Developing tools with robotic process automation or no-code software tools, such as Regrello, will help manage the information flow and provide the basis for good risk evaluation systems.

Implement immediate supplier monitoring

Figure 8: Immediate supplier monitoringDirect suppliers have the highest impact on supply chain performance, and they are affected by their suppliers. Understanding their actual and near-term situation requires certain information (Figure 8), that should be known about suppliers. Companies and suppliers should regularly exchange information on delivery lead-times for ordering. For actual orders, delays should be communicated immediately. Labor and production capacity describe the load problem of the supplier and their impact on delivery times. Material shortages plus supplier geographic dependencies will give a better outlook on supply reliability. This information is typically not available in the purchasing IT systems. Companies need to leverage this information to protectively react by using process automation and information sharing platforms such as Regrello, especially for the high volume of purchase parts.

Figure 8: Immediate supplier monitoringDirect suppliers have the highest impact on supply chain performance, and they are affected by their suppliers. Understanding their actual and near-term situation requires certain information (Figure 8), that should be known about suppliers. Companies and suppliers should regularly exchange information on delivery lead-times for ordering. For actual orders, delays should be communicated immediately. Labor and production capacity describe the load problem of the supplier and their impact on delivery times. Material shortages plus supplier geographic dependencies will give a better outlook on supply reliability. This information is typically not available in the purchasing IT systems. Companies need to leverage this information to protectively react by using process automation and information sharing platforms such as Regrello, especially for the high volume of purchase parts.

Conclusions

Many supply chain managers had to deal with disruptions in the past months and quarters. While many companies have focused on firefighting, a systematic approach is helpful to achieve a robust material supply not only now, but also for the next months.

There are three different time frames to look at:

In the actual situation, the immediate focus is on ensuring supply and dealing with delivery delays.

Short term, possible supply risks need to be identified before they happen. This requires monitoring the markets, the countries and the transport.

In the long-term perspective, many of the decisions of the past need to be reconsidered. Will the advantage of low labor cost in a faraway country be outweighed by transport costs, higher inventory due to longer transport times and supply disruptions?

Many assumptions in the supply chain must be reconsidered based on the new realities, such as transport bottlenecks will not disappear, port capacity cannot be increased endlessly. While it is always easy to defend the status quo, future oriented supply chain managers will not focus only on the day-to-day firefighting, but develop solutions to improve material availability as described above.

The supply chain problems also indicate a new task for the supply chain industry: Data, processes and decisions are required to improve material availability. The existing IT tools are not aligned with the requirements of the actual situation. New tools to support decision making for the supply chain are needed, that will focus on supplier capabilities and the associated risk management.

As with many problems in the past, one can only hope that the actual situation does not become the new normal. But if it were the case, there are key steps that can be taken to improve material supply. Many of them have been described. Some of these are easy to implement, but many need a clear change of strategic directions. Supply chain thought leaders and supply chain practitioners need to continue to work together, to implement a new thinking in the supply chain.

Bibliography

8 Things You Should Know About Water & Semiconductors. (n.d.). China Water Risk. Retrieved May 17, 2022, from https://www.chinawaterrisk.org/resources/analysis-reviews/8-things-you-should-know-about-water-and-semiconductors/

Attinasi, M. G., Balatti, M., Mancini, M., & Metelli, L. (2022). Supply chain disruptions and the effects on the global economy. Economic Bulletin Boxes, 8.

Caniëls, M. C. J., & Gelderman, C. J. (2005). Purchasing strategies in the Kraljic matrix—A power and dependence perspective. Journal of Purchasing and Supply Management, 11(2), 141–155. https://doi.org/10.1016/j.pursup.2005.10.004

Caprani, C. (2018). Genoa bridge collapse a sign of things to come if infrastructure maintenance ignored. https://ipweaq.intersearch.com.au/ipweaqjspui/handle/1/3905

Ford, H. (2019). Today and Tomorrow: Commemorative Edition of Ford’s 1926 Classic. Routledge. https://doi.org/10.4324/9780203735633

Haraguchi, M., & Lall, U. (2015). Flood risks and impacts: A case study of Thailand’s floods in 2011 and research questions for supply chain decision making. International Journal of Disaster Risk Reduction, 14, 256–272. https://doi.org/10.1016/j.ijdrr.2014.09.005

Helper, S., & Soltas, Evan. (n.d.). Why the Pandemic Has Disrupted Supply Chains. The White House. Retrieved May 11, 2022, from https://www.whitehouse.gov/cea/written-materials/2021/06/17/why-the-pandemic-has-disrupted-supply-chains/

How Long Will the Chip Shortage Last? | J.P. Morgan Research. (n.d.). Retrieved May 11, 2022, from https://www.jpmorgan.com/insights/research/supply-chain-chip-shortage

Ji-Hyland, C., & Allen, D. (2022). What do professional drivers think about their profession? An examination of factors contributing to the driver shortage. International Journal of Logistics Research and Applications, 25(3), 231–246. https://doi.org/10.1080/13675567.2020.1821623

Lee, J. M., & Wong, E. Y. (2021). Suez Canal blockage: An analysis of legal impact, risks and liabilities to the global supply chain. MATEC Web of Conferences, 339, 01019. https://doi.org/10.1051/matecconf/202133901019

Ravi, S. (2022, March 3). Global Semiconductor Sales Increase 26.8% Year-to-Year in January. Semiconductor Industry Association. https://www.semiconductors.org/global-semiconductor-sales-increase-26-8-year-to-year-in-january/

Stalk, G. (1992). Time‐based competition and beyond: Competing on capabilities. Planning Review, 20(5), 27–29. https://doi.org/10.1108/eb054375

‘til the Next Zero-Day Comes | Safety-Critical Systems eJournal. (n.d.). Retrieved May 19, 2022, from https://scsc.uk/journal/index.php/scsj/article/view/5

Weathering the Chip Shortage Requires Future-Proofing Supply Chains. (n.d.). Retrieved May 11, 2022, from https://www.supplychainbrain.com/blogs/1-think-tank/post/34617-weathering-the-chip-shortage-and-future-proofing-the-supply-chain

Wendler-Bosco, V., & Nicholson, C. (2020). Port disruption impact on the maritime supply chain: A literature review. Sustainable and Resilient Infrastructure, 5(6), 378–394. https://doi.org/10.1080/23789689.2019.1600961